Three Years to Everywhere

AI crossed 53% adoption in three years. The internet took seven. The test that follows is the same.

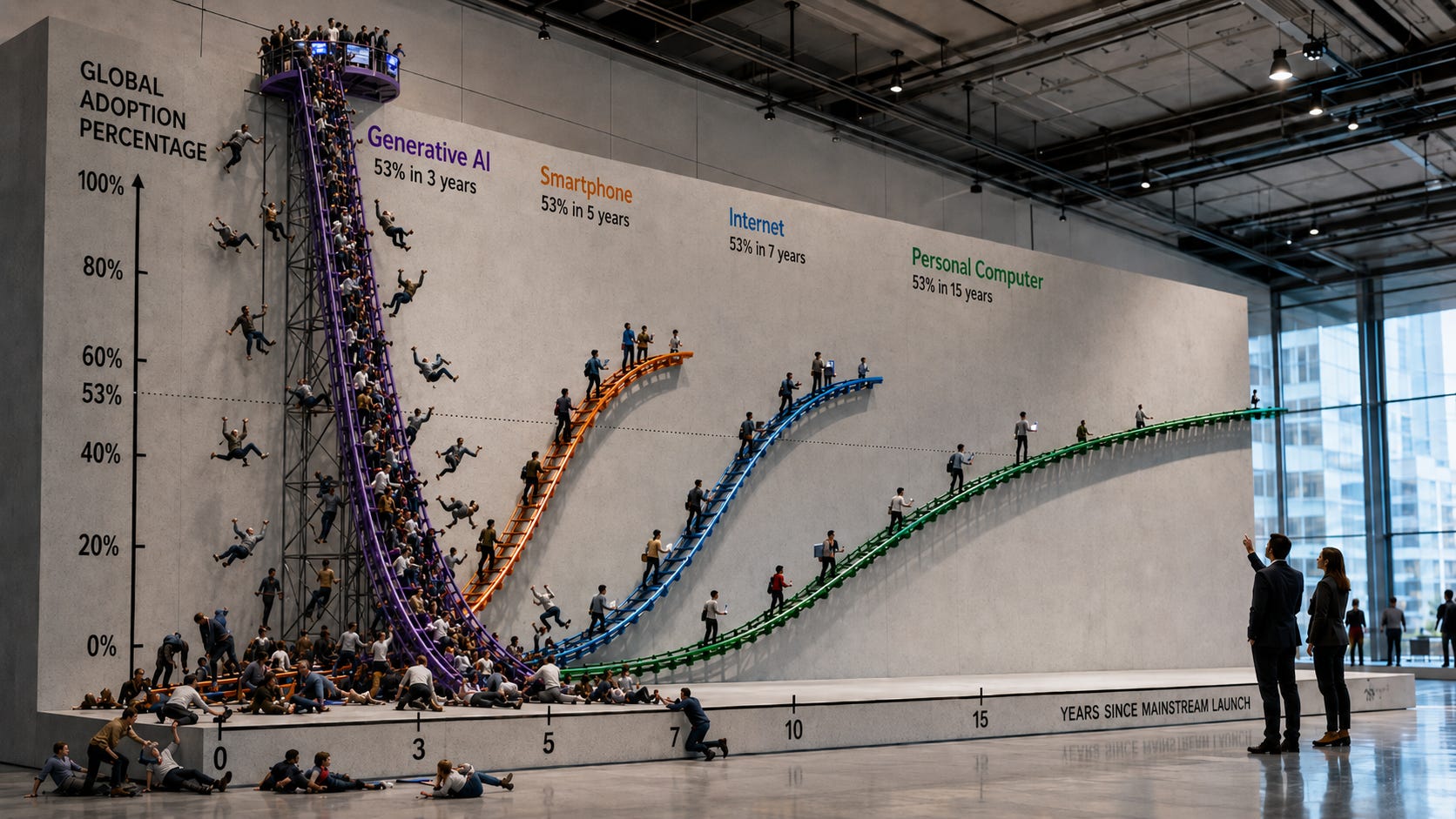

The number is three. Three years from the public launch of ChatGPT in November 2022 to the moment the Stanford HAI AI Index confirmed, in April 2026, that generative AI had crossed 53% adoption among the global connected population. The personal computer took fifteen years to reach the same threshold. The internet took seven. The smartphone took five. No general-purpose technology in recorded history has moved from zero to majority adoption faster.

The number looks like a victory. It is not. It is a diagnostic.

Every general-purpose technology that has reached 53% adoption has faced the same structural test within eighteen months of crossing the line: does usage deepen from novelty into necessity, or does the adoption curve flatten as the gap between early enthusiasm and mainstream reality becomes too wide to bridge? The personal computer reached 53% of American households in the mid-1990s and then plateaued for years, because most owners used it for word processing and solitaire, until the internet arrived and gave it a reason to exist every day. The internet reached 53% around 2001 and then the dot-com crash filtered the casual browsers from the committed users. Adoption dipped briefly before e-commerce, streaming, and social media pulled it back into sustained acceleration. The smartphone reached 53% around 2012, by which point the app ecosystem had matured enough that the device was no longer a phone with features but a computer that happened to make calls.

In each case, the technology needed a second act: a killer application phase that converted exposure into dependency. In each case, the 53% threshold was not the destination. It was the starting gate.

Dario Amodei, the CEO of Anthropic, stood at a press conference on May 6, 2026 and described what the adoption curve looks like from inside a company riding it. Anthropic’s compute demand had grown 80-fold in the first quarter alone, he said, a figure so large it had created what he called “difficulties with compute.” The company’s annualized revenue had crossed $30 billion, surpassing OpenAI. But the growth was not coming from the 53%. It was coming from a narrow band of users, developers and enterprises and researchers, who had moved beyond experimentation into genuine integration. The question Amodei did not address, because it was not yet a problem for his business, was what was happening with everyone else.

The everyone else is where the 53% number starts to fracture. A report published by TechCrunch in March 2026, drawing on subscription analytics from ChartMogul, found that AI-powered apps retain subscribers at an annual rate of 21.1%, compared to 30.7% for non-AI apps. Users churn 30% faster from AI products than from conventional software, despite generating 41% more revenue per customer during the time they stay. The pattern is distinctive: a strong first-use moment followed by a failure to convert trial into habit. Many users try an AI tool, find it impressive, and then discover they have no sustained reason to return.

ChatGPT’s trajectory tells the same story from a different angle. OpenAI reported 900 million weekly active users in February 2026, up from 400 million a year earlier. The headline growth rate, 125% year over year, is staggering. But underneath it, ChatGPT’s share of the AI chatbot market dropped from 69.1% in January 2025 to 45.3% by early 2026, according to app-tracker data reported by Fortune. The market is fragmenting. Users are trying multiple tools. And the conversion from free to paid remains remarkably thin: an estimated 10 to 15 million paying subscribers out of 900 million weekly users yields a conversion rate below 2%. For comparison, Spotify converts 45% of its active users to paid. The gap between those two numbers is the gap between a product people enjoy and a product people need.

GitHub Copilot offers perhaps the cleanest view into what integration actually looks like. Microsoft reported 4.7 million paid subscribers in January 2026, deployed across 90% of Fortune 100 companies. The product works. Developers who use it report measurable productivity gains. But 4.7 million paid subscribers out of 150 million registered GitHub developers is a 3.1% conversion rate. Even among the professional demographic most naturally suited to AI integration, the technically fluent developers who write code for a living, 97 out of 100 have not concluded that AI assistance is worth paying for.

This is the engagement bifurcation the headline adoption number disguises. A small percentage of users, estimated at 10% to 15% of the 53% who have tried generative AI, have genuinely integrated it into daily professional workflows. Developers building with Claude Code or Cursor. Researchers using Perplexity for literature review. Analysts using AI to process earnings transcripts. These power users report transformative productivity gains, and they are disproportionately responsible for the revenue growth at Anthropic, OpenAI, and the other labs. The remaining 85% to 90% of the adoption curve is made up of casual experimenters and one-time tryers, the users who asked ChatGPT to plan a holiday or summarise an article, found the result adequate but not essential, and never developed a daily habit.

The NBER’s February 2026 finding, that more than 80% of companies actively using AI report no measurable productivity impact, is the enterprise-level expression of the same bifurcation. Sixty-nine percent of firms are using AI. Executives personally average 1.5 hours of AI usage per week, according to the NBER survey. But the productivity shows up only at the firms that were already the most productive before AI arrived. For the majority, adoption has occurred. Integration has not.

The historical parallel that matters most is not the smartphone, which is the optimistic case, but the internet circa 2001. At 53% penetration, the internet had email, basic browsing, and a handful of e-commerce sites. It did not yet have the applications that would make it indispensable: broadband streaming, social media, cloud-based productivity tools, mobile integration. Those applications arrived between 2003 and 2007, and they are what converted the internet from something people used occasionally into something people could not function without. The internet’s 53% in 2001 was real adoption, but it was not yet deep adoption. It took a second wave of innovation to make it stick.

Generative AI in May 2026 is structurally analogous. The technology has reached majority exposure. ChatGPT has 900 million weekly users. Google AI Overviews reach 2 billion monthly users by surfacing AI-generated summaries inside ordinary search results. Perplexity processes more than a billion queries per month. The surface-level numbers are extraordinary. But the daily-habit applications, the equivalents of Gmail and Google Maps and Instagram, have not yet arrived for mainstream users. The power users have found their daily habit: coding assistance, research acceleration, content generation. The mainstream has found a novelty they revisit intermittently.

The turn in the historical parallel is that the internet’s trial period at 53% was violently brief. The dot-com crash arrived in 2000 and wiped out $5 trillion in market value within two years. It did not kill the internet. It killed the companies that had mistaken adoption for revenue. The survivors, Amazon, Google, eBay, were the companies whose products had become necessities rather than novelties. The crash was the filter that separated exposure from integration. For generative AI, the equivalent filter is not a market crash but a revenue test: can AI companies sustain the growth rates their valuations require when 85% of their potential market has tried the product and not converted to habitual use?

Amodei’s 80-fold compute growth suggests that for the power user segment, the answer is emphatically yes. Anthropic’s trajectory is real. So is OpenAI’s $24 billion annualized run rate. But both companies are riding a power-law curve in which a small fraction of users generates the overwhelming majority of revenue. The question is whether the rest of the 53% follows, or whether generative AI settles into the pattern of a technology that is transformative for the few and optional for the many. Think of Excel: adopted by virtually every office worker, mastered by a small percentage, and genuinely productivity-transforming only for those who learned to use it beyond basic spreadsheets. An Excel-like outcome would be valuable. It would not justify the $582 billion in global AI investment deployed in 2025.

If you are pricing the AI infrastructure trade over the next eighteen months, four scenarios emerge from the historical framework, and the most probable is not the one the market is pricing.

Forty percent of the probability weight belongs to the smartphone trajectory, the path where generative AI tools improve rapidly enough that the casual user becomes a daily user. Killer applications emerge: AI assistants that manage calendars, finances, and health with genuine reliability. AI tutors that personalise education. AI creative tools that reach professional grade. Adoption deepens from 53% to 70% or higher by 2028. The power user divide narrows as interfaces become simpler and outputs become more trustworthy. This is the world in which the $582 billion pays off on schedule. It requires a second wave of AI product innovation, the equivalent of the app ecosystem that turned the smartphone from a gadget into a utility.

Thirty percent sits with bifurcated integration: the Excel outcome. Power users, roughly 15% to 20% of the population, integrate AI deeply into professional workflows and cannot imagine working without it. Another 30% to 35% use AI casually for specific tasks: travel planning, writing assistance, image generation. The remaining half of the population stops using AI entirely or uses it so infrequently that it never registers as a daily habit. The technology is valuable but not universal. Anthropic and OpenAI sustain strong businesses serving the professional tier. The mass-market consumer AI play never materialises. The capex deployed in 2025 generates returns, but at lower multiples than the market is currently pricing.

Twenty percent goes to plateau and disillusionment. The NBER 80% number persists through 2027. Enterprise deployments fail to produce returns measurable enough to justify renewal. Consumer engagement continues its decline. AI investment slows. The 53% adoption mark becomes the peak of the hype cycle, not a waypoint on the path to ubiquity. AI retreats into specialised professional tools for coding, research, and data analysis, valuable but narrower than the revolution the investment thesis requires.

The final ten percent is the metaverse trajectory, the path where adoption reverses. Regulatory restriction, public backlash, and disappointing results converge. The 53% number drops to 30% to 35% by 2028 as casual users abandon tools that never became habits. AI remains important in enterprise but becomes culturally unfashionable among consumers. The $582 billion in capex produces infrastructure that sits underutilised. This is the catastrophic scenario for AI investors, and it requires a combination of forces that is not yet visible in the data but is not inconceivable given the sentiment trends documented in the Pew, Gallup, and NBC surveys.

The signal that distinguishes the first scenario from the other three is not adoption breadth, which is already at 53%, but engagement depth. Three metrics will tell the story before the investment returns do.

The DAU/MAU ratio across major AI platforms is the engagement vital sign. For social media products, a healthy ratio is 50% or higher, meaning half of monthly users return every day. Current estimates for AI tools suggest 20% to 30%. If this ratio rises above 35% by the end of 2026, the smartphone trajectory is becoming probable. If it falls below 20%, the plateau scenario gains weight.

Paid subscription conversion rates are the willingness-to-pay signal. ChatGPT’s sub-2% conversion and GitHub Copilot’s 3.1% conversion are the baselines. OpenAI’s next quarterly disclosure, expected in the July to August window, will show whether the 900 million user base is converting at a higher rate or whether growth is occurring at the free tier while paid subscribers plateau.

The enterprise productivity surveys, particularly the McKinsey Global AI Survey expected in September 2026, will determine whether the NBER 80% number is a permanent feature of AI adoption or an early-stage artefact. If the number drops below 65%, the investment thesis strengthens. If it holds above 75%, the bifurcated integration scenario becomes the most probable outcome.

The killer-app question remains the wildcard. Every prior technology cycle at 53% adoption required a specific breakthrough application to convert exposure into dependency. The internet had Google and then social media. The smartphone had the App Store. Generative AI has not yet produced its equivalent for the mainstream user. If a breakthrough application emerges in the next twelve months, one that makes AI feel as indispensable as mobile search or ride-hailing, the probability distribution shifts dramatically toward the smartphone trajectory. If no such application emerges, the historical pattern suggests the technology settles into bifurcated integration at best.

Three years to everywhere. The telephone took thirty-five years to reach the same point. The personal computer took fifteen. The internet took seven. Generative AI did it in three. But everywhere is not the same as essential. The internet reached everywhere and then needed six more years and a market crash before it became the infrastructure of daily life. Amodei’s 80-fold growth is real, and it tells you that for a narrow band of users, AI has already become essential. The 53% number tells you that for the majority, it has not. The next eighteen months will determine which number defines the era: the three years it took to arrive, or the percentage that stayed.

ANNEX: WILL THE 53% DEEPEN OR DISSOLVE?

Generative AI has reached majority global adoption faster than any technology in recorded history. The question for anyone pricing the AI infrastructure trade is whether adoption converts to integration. Four scenarios, mutually exclusive and collectively exhaustive, sum to 100%.

Smartphone Trajectory: 40%

If you are long the AI infrastructure buildout and your thesis depends on mass-market AI revenue, this is the scenario you need. AI tools improve rapidly enough that the casual user becomes a daily user. A killer application emerges that makes AI feel as indispensable as mobile search or ride-hailing. The power user divide narrows as interfaces simplify. Adoption deepens from 53% to 70% or higher by 2028. The $582 billion in 2025 capex generates returns on schedule. Enterprise productivity data improves. The NBER 80% number drops below 50% as firms complete the transition from deployment to workflow integration. Consumer sentiment shifts as tangible benefits reach mainstream users.

Tracking variable: ChatGPT DAU/MAU ratio and paid subscription conversion rate, reported quarterly by OpenAI. At one month, probability is 40%. At three months, if DAU/MAU rises above 35%, probability rises to 50%. At twelve months, the September 2026 McKinsey survey and Q4 enterprise earnings calls determine whether this path is confirmed. If the NBER 80% number drops below 65%, probability rises to 55%.

Bifurcated Integration: 30%

If you are an enterprise buyer deciding how much to invest in AI tooling, this is the world you are most likely operating in already. Power users, roughly 15% to 20% of the population, integrate AI deeply and generate the majority of AI company revenues. Another 30% to 35% use AI casually. The remaining half never develops a daily habit. Anthropic and OpenAI sustain strong businesses serving the professional tier at premium pricing. Mass-market consumer AI never materialises as a standalone revenue category. AI infrastructure generates returns, but at cloud computing multiples rather than software multiples. The capex cycle produces infrastructure that is utilised but not at the rates the 2025 investment thesis assumed.

Tracking variable: GitHub Copilot paid subscriber count (next disclosure expected July 2026). If the 4.7 million figure grows to 7 million or higher, integration is deepening in the developer vertical and can be extrapolated. If growth stalls below 6 million, the power user ceiling is real. At twelve months, the ratio of paid to free users across all major AI platforms is the definitive signal.

Plateau and Disillusionment: 20%

If you are modelling AI infrastructure returns on a five-year horizon, this is the scenario that forces a writedown. The NBER 80% number persists through 2027. Enterprise AI deployments cycle through renewal windows and a significant minority do not renew. Consumer engagement declines as the novelty wears off and no killer application emerges. The 53% adoption figure flatlines or marginally declines. AI retreats to specialised professional tools. Capex generates returns below the cost of capital for the marginal data centre.

Tracking variable: AI app annual retention rates, currently at 21.1% per ChartMogul. If this figure drops below 18% by Q1 2027, the plateau scenario’s probability rises to 30%. If it improves above 25%, probability drops to 10%. The McKinsey Global AI Survey in September 2026 is the single most important data release for this scenario.

Metaverse Trajectory: 10%

This is the tail risk. If you are an allocator deciding whether to increase or trim AI exposure, this is the scenario that justifies a hedge. Adoption peaks and reverses. Regulatory restriction, public backlash (52% of Americans more concerned than excited per Pew, 57% of voters say risks outweigh benefits per NBC News), and disappointing results converge. The 53% figure drops to 30% to 35% by 2028. AI remains important in enterprise but loses cultural momentum. The $582 billion capex cycle produces stranded or underutilised infrastructure. This scenario requires a failure across multiple fronts simultaneously and is currently low-probability, but the sentiment data provides a floor for it that did not exist twelve months ago.

Tracking variable: Pew Research biannual AI sentiment survey and Gallup Gen Z AI attitudes. If the Pew concern figure rises above 60% and Gen Z excitement drops below 15%, the tail risk doubles. If public sentiment stabilises or improves, this scenario’s probability drops to 5%.

Sources:

Stanford HAI, “The 2026 AI Index Report,” April 2026.

OpenAI, ChatGPT 900 million weekly active users announcement, February 27, 2026.

CNBC, “Anthropic CEO says 80-fold growth in first quarter explains ‘difficulties with compute,’” May 6, 2026.

TechCrunch, “AI-powered apps struggle with long-term retention, new report shows,” March 10, 2026.

Fortune, “ChatGPT’s market share is slipping as Google and rivals close the gap,” February 5, 2026.

GitHub/Microsoft, Q2 FY2026 earnings, GitHub Copilot 4.7 million paid subscribers, January 28, 2026.

Google, AI Overviews 2 billion monthly users, AI Mode 100 million monthly active users, Q2 2025 announcement.

NBER Working Paper 34836, “Firm Data on AI,” Ivan Yotzov, Jose Maria Barrero, Nicholas Bloom, et al., February 2026.

Pew Research Center, “Key findings about how Americans view artificial intelligence,” March 12, 2026.

NBC News/Hart Research Associates, “Majority of voters say risks of AI outweigh benefits,” March 2026.

Gallup, “Gen Z’s AI Adoption Steady, but Skepticism Climbs,” April 2026.

ChartMogul, “The SaaS Retention Report: The AI churn wave,” 2026.

Disclaimer: This report is published by Scenarica Intelligence for informational purposes only. It does not constitute investment advice, a solicitation to buy or sell any financial instrument, or a recommendation regarding any particular investment strategy. Scenarica Intelligence is not a registered investment adviser or broker-dealer. All scenario probabilities and assessments represent the analytical judgment of Scenarica Intelligence and are subject to change without notice. Past performance of any asset or strategy discussed does not guarantee future results. Readers should conduct their own due diligence and consult with qualified financial advisers before making investment decisions.

Scenarica Premium: The full Scenarica suite includes Geopolitics, Economy, Bitcoin, AI, and Sunday Edition.

Scenarica Intelligence

We don’t predict the future. We price it.

I love this substack but sadly found this article lacking. AI goes way beyond how many people pay for a chat box. AI solved the protein folding for every protein none. Dr. David Sinclair uses AI in his human trial for longevity, which is one of the most oromising paths to reverse aging. And the US government would never let AI advancement slow because China won't. There are so many avenues of AI exponentially expanding beyond chat boxes. AI is what leads to driverless cars (now) and robots (in a couple years) and much, much more.